Mike Mathweg

Email: MMathweg@MilzHealthGroup.com

Milwaukee Office: (262) 299-4904

Madison Office : (608) 960-9905

Direct Line /Text/SMS: (608) 665-1823

Website: https://milzhealthgroup.com/

Connect with us

Mike Mathweg

Email: MMathweg@MilzHealthGroup.com

Milwaukee Office: (262) 299-4904

Madison Office : (608) 960-9905

Direct Line /Text/SMS: (608) 665-1823

Website: https://milzhealthgroup.com/

Connect with us

Medicare Part A

Hospital Insurance

- Most people don't pay a monthly premium

- Inpatient hospital care

- Inpatient mental health care

- Skilled nursing services

- Hospice care

- Some blood transfusions

- $1,632 deductible/admission for a hospital stay of fewer than 60 days

- Stays of more than 60 days require additional daily copays

- Multiple stays may mean multiple deductibles

- Visit any qualified hospital in the U.S. that accepts new Medicare patients

- Hospital care outside the U.S. isn't usually covered

Medicare Part B

Doctor & Outpatient Visits

- $174.70 monthly premium (may be higher based on income)

- Physician services

- Outpatient hospital services

- Ambulance

- Outpatient mental health

- Laboratory services

- Durable medical equipment (wheelchairs, oxygen, etc.)

- Outpatient physical, occupational therapy

- Some preventive care

- You can get care throughout the U.S., but generally not outside the country

- Participating physicians who accept Medicare patients

- $240 annual deductible for 2024

- Medicare pays 80%, you pay 20% of Medicare-approved cost

- No Maximum-Out-of-Pocket (MOOP)

- No RX Coverage

Medicare Supplement (Medigap)

- Designed to cover what Medicare Parts A & B doesn't – such as deductibles, co-payments, and co-insurance.

- Plans are named A, B, C, D, F, G, K, L, M, N and HDF (except WI, MN, MA).

- Pay-Upfront Type of Plan

Pros

- If plan is put together correctly you will have little to no out-of-pocket costs for medical care.

- Goes with you anywhere in the U.S.

- No networks.

- Guaranteed renewable as long as you pay your premium on time and not made any material misrepresentation on your application for insurance.

Cons

- Premium at age 65 starts at $160+ per month. The more comprehensive coverage, the higher the premium.

- In most cases, premiums are based on gender, ZIP code and age.

- Average increase: 6-7%/year.

- Premiums nearly double every 10 years.

- No RX Coverages included

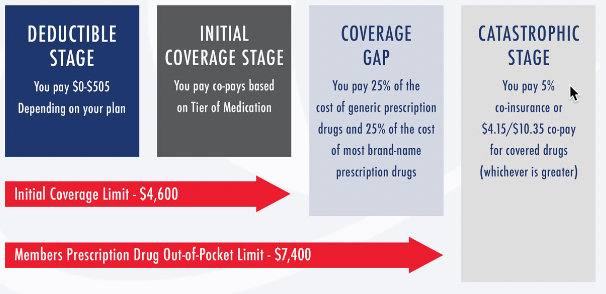

Medicare PDP (Part D)

- Helps with cost of outpatient prescription drugs

- Only offered through private insurance companies

- Most states have 25-30 plans

- Each plan has a list of drugs it covers (formulary)

- Make sure your drugs are covered before you enroll in the plan. The list of

drugs changes yearly. - Coverage is not automatic.

- Penalties may apply if you enroll late (1% per month accumulating).

- Average cost for Part D is $35-45 per month

Option 2: Medicare Advantage (Part C)

- Combines Part A and Part B and, in most cases, includes Part D into one plan

- Offered by private insurance companies (HMO PPO, PFFS, SNP, MSA-No RX)

- Pay-As-You-go Type of Plan

Pros

- Plan premiums start as low as $0 per month

- Eliminate all deductibles associated with Medicare Part A and Part B

- Pay a small copay for all Medicare-covered services

- All plans have a max-out-of-pocket

- Some plans offer additional benefits not covered by Medicare like dental and vision preventive care and gym memberships

Cons

- Most plans use networks of doctors and hospitals.

- Coverage may be limited outside the networks unless emergency room (ER) or urgent care.

- Possible to spend more if you reach out-of-pocket (OOP) maximum.